Amazon seller insurance is a contractual requirement, not just a good idea. Under Amazon's Business Solutions Agreement, sellers who cross Amazon's sales threshold, or who are asked directly, must carry commercial liability insurance and provide a valid certificate of insurance. This guide covers when the requirement triggers, what the policy needs to include, why certificates get rejected, and how to run the process so you are not scrambling after a Seller Central notice.

A note before the details: this is operational guidance about Amazon's compliance workflow, not insurance, legal, or tax advice. Coverage decisions belong with a licensed insurance professional who can see your products and your risk.

Key Takeaways

- Amazon's insurance requirement is in the Business Solutions Agreement. It triggers when your gross sales exceed Amazon's stated threshold, commonly referenced as $10,000 in gross proceeds in one month on Amazon.com, or whenever Amazon requests proof. Verify the current wording in your own Seller Central account.

- The expected coverage is commercial general liability, umbrella, or excess liability written to Amazon's specifications, with Amazon named as an additional insured.

- Most certificate of insurance rejections are clerical: the insured name does not exactly match the Seller Central legal entity, the additional-insured wording is wrong, or dates and limits are off.

- Amazon has stated it may directly pay certain valid customer property-damage and personal-injury claims under $1,000 for sellers who follow policies and hold valid insurance. That concession is not a substitute for coverage.

- Insurance transfers certain covered risk. It does not remove seller responsibility for product safety, and it is subject to exclusions, limits, and deductibles.

When Does Amazon Require Seller Insurance?

The requirement lives in the insurance section of Amazon's Services Business Solutions Agreement, the contract every seller accepts. The commonly referenced trigger for Amazon.com is exceeding $10,000 in gross proceeds in sales in a single month, after which sellers are expected to obtain and maintain commercial liability insurance within 30 days. Amazon can also simply request proof of insurance regardless of the threshold.

Two practical points follow from that:

First, check your own account rather than blog posts, including this one. The threshold wording, the time allowed, and the upload location are defined by the current agreement and your Seller Central Insurance page, and Amazon adjusts contract language over time.

Second, do not wait for the notice. A seller trending toward the threshold has a predictable compliance event coming. Getting quotes, binding coverage, and producing a clean certificate takes days to weeks. Starting after Amazon asks is how sellers end up rushing a non-compliant certificate through and getting it rejected.

Not maintaining required insurance is a contract compliance issue, and unresolved compliance issues can affect selling privileges. Avoid assuming a specific enforcement outcome; the operational answer is simply to stay compliant.

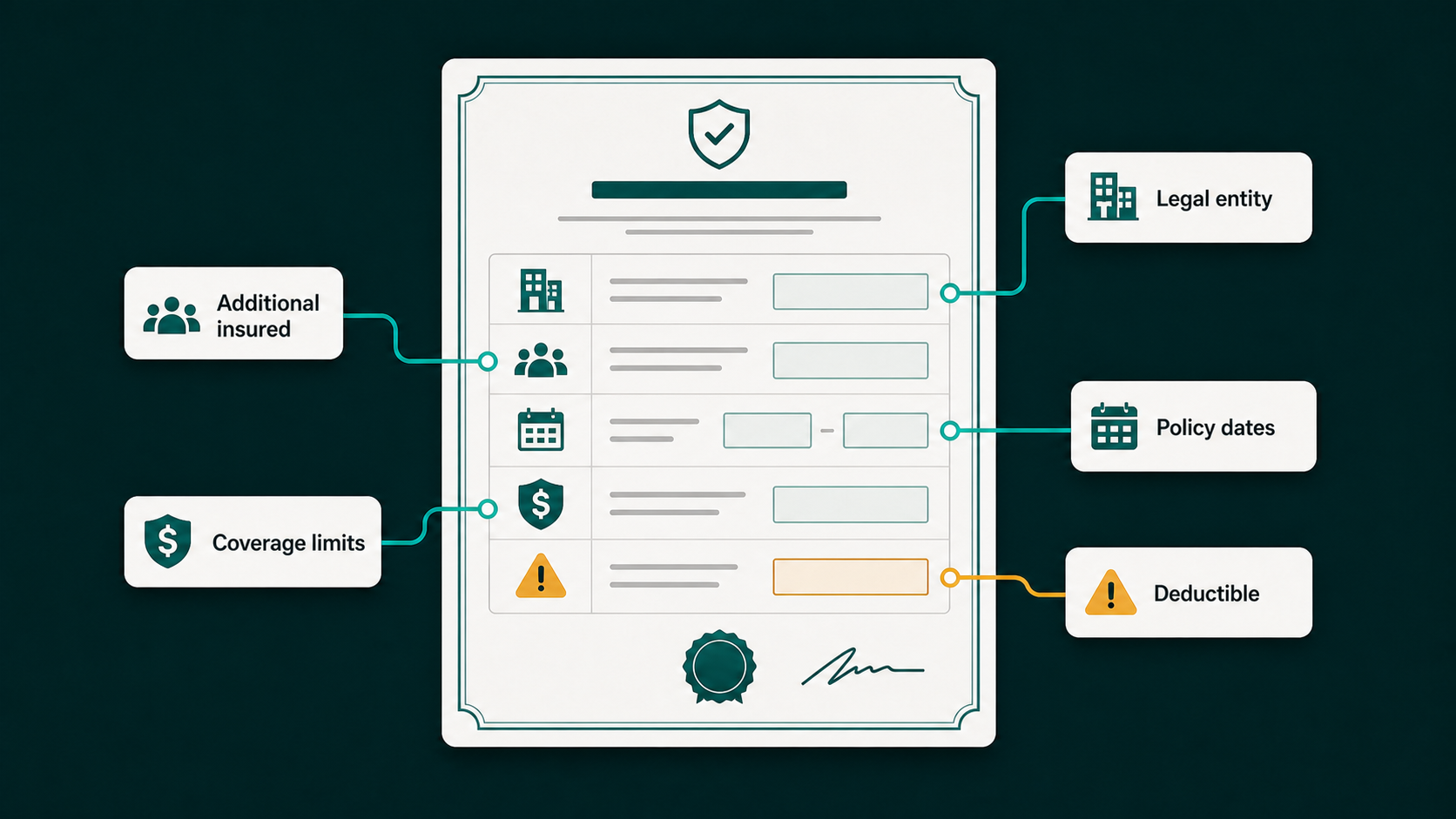

What the Policy Needs to Cover

Amazon's agreement references commercial general liability, umbrella, or excess liability insurance covering liabilities caused by or occurring in conjunction with your business operations, including products and completed operations, bodily injury, and property damage. Amazon and its assignees must be named as additional insureds.

In practice, sellers and their brokers work from a checklist like this. Exact figures and wording must be verified against the current agreement and your Seller Central Insurance page:

| Requirement area | What Amazon has expected | Common failure |

| Policy type | Commercial general liability, umbrella, or excess liability | Claims-made form where occurrence form is expected |

| Limits | Minimum per-occurrence and aggregate limits set by the agreement | Limits below the stated minimum |

| Additional insured | Amazon entities named with Amazon's required wording | Paraphrased or missing wording |

| Named insured | Exactly the legal entity on the selling account | Trade name or punctuation mismatch |

| Coverage scope | All products listed in the Amazon store where you sell | Category exclusions that carve out your actual products |

| Policy dates | Active policy with required remaining validity | Certificate submitted near expiry |

| Deductible | Within the cap stated in the agreement, shown on the certificate | Deductible omitted from the certificate |

The single most useful move: send your insurance agent the actual insurance requirements from your Seller Central account and ask them to build the certificate to that text. Brokers who work with marketplace sellers do this routinely. Generic certificates produced without the Amazon-specific wording are the main source of rejection loops.

Coverage types in plain terms

Commercial general liability (CGL) is the foundation. It is the policy type that responds to third-party bodily injury and property damage claims, including products and completed operations claims, which is the core exposure for anyone selling physical products.

Umbrella and excess liability sit on top of the CGL and add limit. Sellers in higher-risk categories, or sellers whose revenue makes the base limit feel thin, use these layers to extend protection.

Other coverage such as product recall expense, cargo or stock coverage for inventory in transit and at 3PLs, cyber liability, and workers compensation may be relevant to your business. Whether they are worth buying is a conversation for your broker, not something a blog can answer for you.

Why Certificates of Insurance Get Rejected

The certificate of insurance (COI) is the document you upload to Amazon, and it fails for boring reasons:

- Entity mismatch. The insured name reads "Acme Goods" while Seller Central says "Acme Goods LLC". Or the comma is missing. Match the legal entity exactly, character for character.

- Additional-insured wording. Amazon expects its entities named as additional insureds using the wording in the current requirements. Paraphrases get bounced.

- Wrong policy form. Where the requirement specifies the policy form, a different form will not pass review.

- Dates. Lapsed policies, policies that expire too soon after submission, or effective dates that have not started yet.

- Missing data. Deductible not shown, limits not itemized, or product coverage scope unclear.

When a COI is rejected, get the rejection reason, forward it to your agent verbatim, and have the certificate reissued. Do not resubmit the same document hoping for a different reviewer.

What About Customer Injury Claims?

Amazon has publicly described a process under the A-to-z Guarantee for property damage and personal injury claims caused by defective products sold in its store. Amazon has said it may directly pay valid claims under $1,000, at no cost to sellers, when the seller follows policies and holds valid insurance, and that sellers remain responsible for product safety, valid insurance, and valid claims above that.

Read that as an incentive structure: maintaining valid insurance is part of what keeps small claims from landing on your desk, and larger claims are exactly what the liability policy exists for. Do not read it as Amazon insuring your business. It does not.

A Compliance Workflow That Does Not Scramble

- Watch the trigger. If monthly gross proceeds are approaching the threshold in your agreement, start the insurance process now.

- Pull the exact requirements from Seller Central and the current Business Solutions Agreement.

- Brief a broker who knows marketplace sellers. Provide your product list, categories, estimated revenue, prior claims if any, and the Amazon requirement text.

- Bind coverage and request the COI built to Amazon's wording: exact entity name, additional-insured language, limits, dates, deductible.

- Upload through the Insurance section in Seller Central and keep a copy in your compliance records.

- Calendar the renewal 45 to 60 days ahead so there is no lapse, and re-upload the renewed certificate.

- Update the broker when things change: new product lines, new marketplaces, revenue jumps. An outgrown policy is a quiet gap.

Mini-Scenario: The Comma That Took Three Weeks

A kitchenware seller crossed the sales threshold and bought a compliant liability policy the same week. The certificate still bounced twice. First rejection: the insured name showed the brand's trading name instead of the LLC name on the selling account. Second rejection: the reissued certificate fixed the name but dropped the additional-insured wording in the process. The third version, built directly from the requirement text the seller finally copied out of Seller Central and emailed to the agent, passed. Nothing about the coverage ever changed. Three weeks of back-and-forth were purely document mechanics, which is why the requirement text should go to the agent on day one.

FAQ

Do all Amazon sellers need insurance?

The contractual requirement triggers at Amazon's stated sales threshold or on Amazon's request. Sellers below the threshold are not exempt from risk, only from the proof requirement, and many carry coverage anyway. Check the insurance section of your agreement and Seller Central for the wording that applies to your account.

How much does Amazon seller insurance cost?

Premiums depend on product risk, category, revenue, claims history, limits, and the carrier. Anyone quoting a universal number without seeing your business is guessing. Get quotes from brokers who handle e-commerce sellers, and compare what is actually covered, not just price.

What is the Amazon Insurance Accelerator?

Amazon has offered a program connecting sellers with vetted insurance providers familiar with its requirements. Availability, providers, and placement inside Seller Central change, so check the Insurance section of your account for the current options.

Does an LLC replace insurance?

No, and insurance does not replace an entity structure either. They address different problems. Entity and tax questions belong with your attorney and accountant; this article is not legal or tax advice.

Why does Amazon need to be an additional insured?

The Business Solutions Agreement requires it. Naming Amazon as an additional insured extends certain protections of your policy to Amazon for claims arising from your products. Your agent handles the wording; your job is to give them Amazon's exact required text.

What happens if I do not provide insurance when asked?

Failing to meet a contractual requirement creates a compliance problem on the account, and unresolved compliance problems can affect selling privileges. The practical answer is not to test the enforcement path: the coverage that satisfies the requirement is also the coverage that protects the business.

Keeping the Insurance File Boring

Seller insurance compliance is a document discipline problem more than an insurance problem. Know your trigger, give the broker Amazon's exact text, match the entity name to the character, and renew before expiry. Done that way, the insurance file stays boring, which is what a compliance file should be.

If account health notices, compliance requests, or Seller Central case backlogs are taking up your team's week, it helps to treat insurance as part of the broader compliance file rather than a one-off document upload. Qubeq's Amazon account management work covers that kind of operational follow-through before it becomes urgent.